New HWWI-Forecast

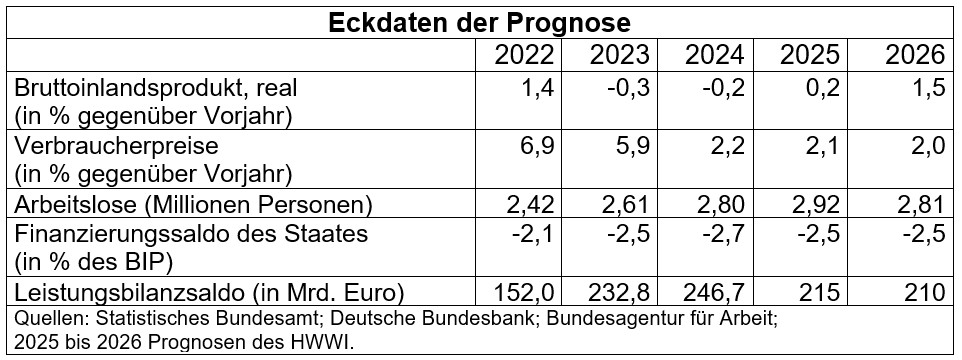

The German economy grew surprisingly significantly in the first quarter of this year, by 0.4%. As some one-off effects favoured this development, the second quarter is likely to be weaker. In the meantime, a new government is in office. The Union had announced comprehensive economic reforms. However, it remains to be seen to what extent the necessary measures to improve the location conditions can be implemented in the coalition with the SPD in view of partly different economic policy ideas. With clear reform decisions, the previous reluctance, especially among investors, is likely to dwindle. The new coalition government has also greatly expanded the debt possibilities for the infrastructure and defense sectors even before taking office. This will provide economic stimulus in the future. In the short term, however, there are still dampening influences. In addition to the geopolitical uncertainties, there is the unpredictable trade policy of the new US administration; tariffs have also been increased or introduced on German exports to the USA, and there is a threat of more. This reduces the economic revival expected for the rest of the year. For 2025, the HWWI expects real gross domestic product to grow by 0.2% on an annual average, not least because of the negative overhang from 2024. Assuming that the new government quickly implements important economic reforms, starts additional spending on infrastructure and defense, and further monetary easing, economic growth of 1 1/2% is possible for 2026.

At 2.1%, the consumer price inflation rate almost reached the stability mark of 2% again in April and May. However, the significant increase in labour costs keeps the so-called core rate – most recently around 2 3/4% – even higher. In the further course, however, inflationary pressures are likely to ease further with more moderate wage settlements and the inflation rate should stabilise at 2%.

It is not only because of the geopolitical uncertainties and the erratic US tariff policy that the risks for this forecast remain high. The economic policy turnaround expected by the new government is still pending, and the less consistently reforms are carried out to improve location conditions, the more limited the growth opportunities.

Press Contact

Contact

Prof. Dr. Michael Berlemann