New HWWI Business Cycle Forecast

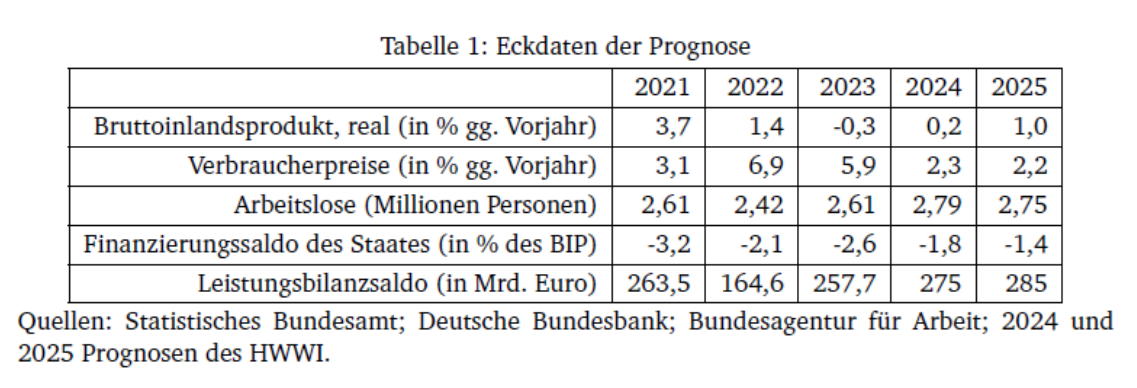

After a small gain in the first quarter of this year, the German economy suffered another slight setback in the second quarter. Overall, the German economy has been “bobbing around” without a clear direction since the beginning of 2022, after the coronavirus-related slump was made up for. Industry and the construction sector remain in crisis; investments are falling. Economic hopes are focused on private consumption. The real incomes of private households and thus their purchasing power have now risen noticeably again, although this has mainly been channelled into savings due to increased uncertainty. With a further increase in real income and a normalization of the propensity to save, private consumption should at least pick up. The Hamburg Institute of International Economics (HWWI) therefore continues to expect a slight recovery for the German economy in the remainder of 2024 and then again in 2025; economic growth is likely to average 0.2% in 2024 and 1% in 2025.

At 1.9%, the rate of inflation for consumer prices fell just below the stability mark of 2% again in August, albeit partly thanks to base effects and favorable fuel prices and therefore probably only temporarily for the time being. The core inflation rate is still at 2.8%. It is likely to remain difficult to reach the stability mark in the long term because, on the one hand, prices at the upstream levels have reversed since the start of the year; they are mostly rising again. In addition, the significant rise in service prices as a result of higher wages is slowing down the disinflation process. The consumer price index is expected to rise by an average of just over 2% in both 2024 and 2025. The ongoing geopolitical uncertainties pose a number of risks for the global economy, and therefore also for these forecasts. And the planned Growth Opportunities Act can only be a first step towards improving the domestic framework conditions. Under these conditions, the expected recovery process is also likely to be rather bumpy.

Press Contact

Contact

Prof. Dr. Michael Berlemann